An irreverent Wall Street Blog

SEC Grants FINRA An Extraordinary Voluminous Extension

March 19, 2015

Good for the goose, good for the gander. Or so it is said. For those of us who practice law, we know that there are always exceptions, explanations, and excuses as to why turnaround is not always fairplay. Few things in law are more enervating and disheartening than to be confronted with a tilted playing field that the groundskeepers swear is level. Sometimes you have to break the rules because justice and fairness compel such a wink. I've demanded such consideration and compassion on behalf of clients. On the other hand, sometimes it just seems like there's an old-boys' network of secret handshakes, and rules get interpreted in odd ways that favor those in power to the detriment of those lacking the right connections. Rather than be accused of spinning a recent issue to make the

inexplicable seem more absurd, let me quote the entire Securities

and Exchange Commission ("SEC") release:

UNITED STATES OF AMERICA

Before the SECURITIES AND EXCHANGE COMMISSION

SECURITIES EXCHANGE ACT OF 1934Release No. 74527 / March 18, 2015ADMINISTRATIVE PROCEEDING File No. 3-16424In the Matter of LEK SECURITIES CORPEXTENSION ORDERThe Financial Industry Regulatory Authority ("FINRA") has requested an extension of time to file the certified record, now due March 20, 2015. FINRA cites they did not maintain the voluminous record and it contains approximately 15,000 pages. Extensions of time are disfavored. It appears appropriate, however, to grant FINRA's request. Therefore,It is ORDERED that the time for filing the certified record is extended to April 1, 2015.For the Commission, by its Secretary, pursuant to delegated authority.Lynn M. Powalski Deputy Secretary

SEC Release at http://www.sec.gov/litigation/admin/2015/34-74527.pdf

Content and Context

Lemme see if I got

this. Lek Securities has appealed some Financial Industry Regulatory

Authority ("FINRA") regulatory matter to SEC. As to what the

appealed-from FINRA matter is, we are not told in the SEC Order.

You'd think that the SEC would have provided us with some content and context

so that we knew just what the hell was going on but, hey, all that I can do is

rant.

SIDE BAR: Could it be one of these FINRA matters being appealed to the SEC?

Lek Securities Corporation (CRD #33135, New York, New York) was censured and fined $100,000. The sanctions were based on findings that the firm failed to establish and implement AML policies and procedures, and internal controls that could be reasonably expected to detect and cause the reporting of suspicious transactions and that were reasonably designed to achieve compliance with the Bank Secrecy Act and the implementing regulations promulgated by the Department of the Treasury. The findings stated that the firm depended upon an ad hoc, undocumented, manual system of surveillance for potential wash trades and other types of manipulative activities that was inadequate in the high-volume electronic trading environment in which the firm operated. Although the firm later instituted new surveillance procedures and mechanisms, its approach to its AML responsibilities remained inadequate in design and implementation since it did not document the actual review, investigation and determination with respect to any particular potential suspicious trading, and did not specify the procedures for investigating suspicious trading and determining whether a suspicious activity report (SAR) should be filed. The findings also stated that the Department of Enforcement failed to prove that the firm's supervisory systems and WSPs relating to portfolio margining for a particular customer violated NASD®/FINRA rules. As a result, that allegation was dismissed.This matter has been appealed to the NAC and the sanctions are not in effect pending review. (FINRA Case #2009020941801).

Page 31 - 32 of FINRA's March 2015 "Disciplinary and Other FINRA Actions" Report

SEE FINRA Department of Enforcement, Complainaint, v. Lek Securities Corporation and Samuel Frederik Lek, Respondent (OHO Decision, Disciplinary Proceeding No. 2009020941801 / December 30,2014):

The Respondent Firm failed to establish and implement anti-money laundering policies and procedures that were reasonably designed to achieve compliance with the Bank Secrecy Act and the implementing regulations promulgated by the Department of the Treasury. This misconduct violated NASD Conduct Rules 3011(a) and 2110 and FINRA Rules 3310(a) and 2010, as alleged in the First Cause of Action. For this misconduct, the Firm is censured, fmed $100,000, and ordered to pay costs.The Department of Enforcement failed to prove that Respondents' supervisory systems and written supervisory procedures relating to portfolio margining for a particular customer violated NASD Conduct Rules 3010 and 2110 and FINRA Rule 2010, as alleged in the Second Cause of Action. That Cause ofAction is dismissed.Page 1 of the OHO Decision

The Record

In any event, here's what's

bothering me. When a Respondent in a FINRA regulatory hearing is

found guilty, the self-regulatory organization ("SRO") imposes

sanctions, which frequently include the costs of the administration of the hearing

and the cost of the transcript. Normally, inherent in those charges is the cost

of preparing the ongoing record of the case. The reason that a record is

prepared is to provide something for an appellate body (regulators and/or

courts) to review should a decision be appealed. In this day and age,

preparing a record isn't quite the ordeal that it used to be. With all the

PDFing and MP3ing that has taken over so much of hard-copy content and oral

testimony, it's more a question of assembling digital files rather than the

old-fashioned photocopying and transcribing tapes.

SIDE BAR: Note how the charges for administering the hearing and maintaining a transcript are often set forth:In FINRA Department of Enforcement, Complainaint, v. Lek Securities Corporation and Samuel Frederik Lek, Respondent (OHO Decision, Disciplinary Proceeding No. 2009020941801 / December 30,2014) [Ed: highlighting provided]:For failing to establish and implement anti-money laundering policies and procedures that were reasonably designed to achieve compliance with the Bank Secrecy Act and its implementing regulations, in violation of NASD Conduct Rules 3011(a) and 2110 and FINRA Rules 3310(a) and 2010, as alleged in the First Cause of Action, Lek Securities Corporation is censured, fined $100,000, and ordered to pay costs. The costs are in the amount of $14776.34, which includes a $750 administrative fee and the cost of the transcript.184 The fine and assessed costs shall be due on a date set by FINRA, but not sooner than thirty days after this decision becomes FINRA's final disciplinary action in this proceeding.Page 46 of the OHO Decision

SEC Rules of

Practice

Now, consider the SEC's

Rules of Practice, in particular [Ed: highlighting

supplied]:

Rule 420. Appeal of Determinations by Self-Regulatory Organizations.(a) Application for Review; When Available. An application for review by the Commission may be filed by any person who is aggrieved by a determination of a self-regulatory organization with respect to any

(i) final disciplinary sanction;(ii) denial or conditioning of membership or participation;(iii) prohibition or limitation in respect to access to services offered by that self-regulatory organization or a member thereof; or (iv) bar from association as to which a notice is required to be filed with the Commission pursuant to Section 19(d)(1) of the Exchange Act, 15 U.S.C. 78s(d)(1).

(b) Procedure. As required by section 19(d)(1) of the Securities Exchange Act of 1934, 15 U.S.C. 78s(d)(1), an applicant must file an application for review with the Commission within 30 days after the notice of the determination is filed with the Commission and received by the aggrieved person applying for review. The Commission will not extend this 30-day period, absent a showing of extraordinary circumstances. This rule is the exclusive remedy for seeking an extension of the 30-day period.(c) Application. The application shall be filed with the Commission pursuant to Rule 151. The applicant shall serve the application on the self-regulatory organization. The application shall identify the determination complained of and set forth in summary form a brief statement of the alleged errors in the determination and supporting reasons therefor. The application shall state an 8 address where the applicant can be served. The application should not exceed two pages in length. If the applicant will be represented by a representative, the application shall be accompanied by the notice of appearance required by Rule 102(d).(d) Determination Not Stayed. Filing an application for review with the Commission pursuant to paragraph (b) of this rule shall not operate as a stay of the complained of determination made by the self-regulatory organization unless the Commission otherwise orders either pursuant to a motion filed in accordance with Rule 401 or on its own motion.(e) Certification of the Record; Service of the Index. Fourteen days after receipt of an application for review or a Commission order for review, the self regulatory organization shall certify and file with the Commission one copy of the record upon which the action complained of was taken, and shall file with the Commission three copies of an index to such record, and shall serve upon each party one copy of the index.

Extraordinary

Circumstances

Imagine that you are an

aggrieved FINRA Respondent and intend to appeal to the SEC. The SEC

Rules of Practice isn't exactly all warm and bubbly concerning your

deadline. You got 30-days from notice of FINRA's determination. Trust me (and

you can look it up), if you don't file within the 30-days, FINRA will be all up

your . . . well, you can imagine. Also, note how inflexible the SEC is in terms

of any excuses for a late appeal: The Commission will not extend this 30-day period,

absent a showing of extraordinary

circumstances.

SIDE BAR: In the Matter of the Application of Caryl Trewyn Lenahan for Review of Disciplinary Action Taken by FINRA (SEC Order Granting Motion To Dismiss Application for Review, '34 Act Release No. 73146; Admin. Proc. File No. 3-15833 / September 19, 2014), FINRA moved to dismiss Respondent Lenahan's appeal to the SEC. FINRA, which had barred Lenahan for failing to respond to its investigative requests, argued that her appeal to the SEC was filed about 18 months beyond Rule 420's 30-day deadline. In granting FINRA's Motion and finding Lenahan's appeal untimely, the SEC asserted:Even if Lenahan had exhausted her administrative remedies, we must dismiss her application for review because it was untimely. Under Section 19(d)(2) of the Securities Exchange Act of 1934, an applicant has thirty days to submit an application to the Commission for review of a disciplinary action imposed by a self-regulatory organization. 11 Lenahan's application was due October 25, 2012, but she waited until April 10, 2014, to file. Only in extraordinary circumstances does the Commission provide an exception for late filings, 12 and Lenahan has failed to show any extraordinary circumstances here. 13 Her professed ignorance of the bar's consequences and alleged reliance on advice from a FINRA examiner-the only reasons she offers for the untimeliness of her application-do not constitute extraordinary circumstances that would excuse her late filing.14 Lenahan's application is thus properly dismissed on this ground as well.Page 5 of the SEC Order

Certify And

File

About the only obligation imposed upon FINRA

under the SEC Rules of Practice as part of the preliminary

filing of a respondent's appeal with the SEC is that 14 days after the federal

regulator gets the appeal, the self-regulatory organization shall certify and file with the Commission one

copy of the record upon which the action complained of was taken, and shall

file with the Commission three copies of an index to such record, and shall

serve upon each party one copy of the index.

Voluminous

Keeping the SEC Rules

of Practice in mind, we are informed by the federal regulator that

FINRA didn't maintain the "voluminous" record of the Lek hearing. Why

didn't the SRO maintain the file -- which it is required to do and for which it

likely charged the Respondent? Why does the SEC Order use the term "voluminous"

-- I see no reference to

"minimal" or "voluminous" files in SEC Rule of Practice

420(e).

15,000

Pages

Further, assuming that Lek Securities

was charged hearing and transcript costs by FINRA, how is it that FINRA took

the money but, gee, didn't maintain the record? What the hell happened to and

where the hell did 15,000 pages disappear to -- or were they not maintained in

the first place?

Appropriate

Then there's that really troubling

comment in the SEC's release that: It appears appropriate, however, to

grant FINRA's request.

That's the standard for

adjudicating the inability of FINRA to timely file a record on appeal? The SEC

now gets all touchy-feely when it comes to FINRA and if the SEC's Secretary

(mind you, apparently not an Administrative Law Judge) deems it

"appropriate" to release the SRO from compliance with a basic

obligation under SEC Rule of Practice 420, then, so be it? Note that there's

nary a word as to what was presented by FINRA in support of its request for an

extension and there's nary a word as to what was deemed the persuasive

factor(s).

14 Days and 15,000

Pages

Assuming turnaround is fairplay,

what exactly were the "extraordinary circumstances" presented by

FINRA to the SEC in support of the self-regulator's failure to timely certify

the record within the 14-day period proscribed in Rule 420? Assuming the disclosure of that explanation

would not constitute divulging a matter of national security, on what basis is

the rationale for granting the extension not required to be disclosed in the

SEC's published

Order?

Tip Of An

Iceberg?

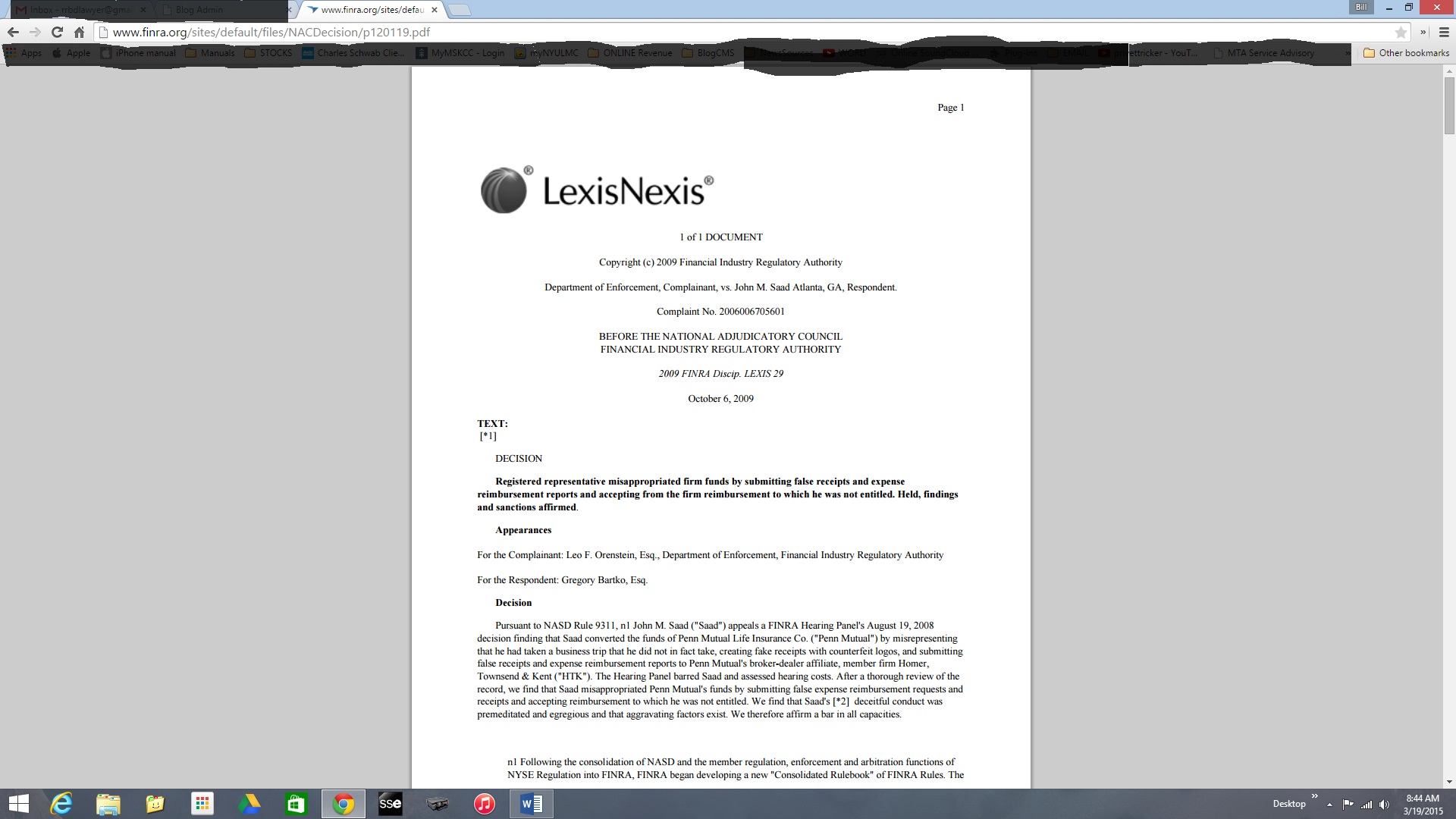

The other day I reported about a

FINRA regulatory matter that had been appealed to the SEC: "The

Amazing Mobius Strip Of Wall Street Regulation" (BrokeAndBroker.com Blog, March 18, 2015). In researching

that article about Respondent Saad, I kept looking for FINRA's official copy of

the relevant National Adjudicatory Council Decision but for

some odd reason, all that the FINRA had posted online was a

LexisNexis

copy of that document -- something that I don't recall seeing in the

past.

{kind=link}

Is

FINRA missing more than just a single 15,000 page

record?

Bill Singer's Comment

SEC Commissioner Daniel Gallagher and I have maintained an

ongoing public dialog on a number of provocative topics, including the future

of FINRA and self-regulation:

- SEC Commissioner Gallagher Says FINRA. Bill Singer Says Finito (BrokeAndBroker.com Blog, September 18, 2014)

- SEC Commissioner Gallagher Takes A Sledge-O-Matic To Wall Street Regulation (BrokeAndBroker.com Blog, May 16, 2014)