An irreverent Wall Street Blog

Permanent Bar Proves Less Than Permanent As SEC Approves Return to Industry

October 29, 2020What's the difference between a regulatory Bar and a regulatory Suspension? Many would answer that a Bar begins on a date certain but does not end on a date certain; whereas, a suspension begins on a date certain and ends on a date certain. With some suspensions, however, you become subject to a statutory disqualification, which, if you think about it, is a variation on the theme of a bar. Nonetheless, the general idea behind a Bar is that you're out of the business. Can you get back in? Sometimes, yes. Sometimes, no. It all sort of depends. Depends on what exactly? Ahhh . . . now there's the rub. Consider the petitions to the Securities and Exchange Commission by a barred individual.

2011: SEC Wanger OIP

As with most things that are SEC regulatory matters, we start with an Order Instituting Administrative Proceedings; and, as such, in the case of one respondent, Eric David Wanger, we begin with: In the Matter of Eric David Wanger and Wanger Investment Management, Inc., Respondents. (Order Instituting Administrative and Cease-and-Desist Proceedings Pursuant to Section 8a of the Securities Act, Section 21c Of The Securities Exchange Act, Sections 203(E), 203(F) and 203(K) off the Investment Advisers Act of 1940, and Section 9(B) of the Investment Company Act Of 1940; '33 Act Rel. No. 9288; '34 Act Rel. No. 66053; Invest. Adv. Act Rel. No. 3342; Invest. Co. Act Rel. No. 29893; Admin. Proc. File No. 3-14676 / December 23, 2011) ("the OIP"). The SEC News Digest (Issue 2011-247, December 23, 2011) offered this synopsis:

In the Matter of Eric David Wanger and Wanger Investment Management Inc.On December 23, 2011, the Commission issued an Order Instituting Administrative and Cease-and-Desist Proceedings Pursuant to Section 8A of the Securities Act of 1933, Section 21C of the Securities Exchange Act of 1934, Sections 203(e), 203(f) and 203(k) of the Investment Advisers Act of 1940 and Section 9(b) of the Investment Company Act of 1940 (Order) against Eric David Wanger (Wanger) and Wanger Investment Management Inc. (Wanger Management).In the Order, the Division of Enforcement (Division) alleges that Wanger and Wanger Management repeatedly marked the closing price of certain stocks held by the Wanger Long Term Opportunity Fund II, LP (Fund) to artificially inflate the Fund's performance results in an attempt to attract new investors and keep current investors. The Division also alleges that Wanger and Wanger Management engaged in wrongful principal securities transactions with the Fund to repay unauthorized transfers of funds from the Fund's account to Wanger Management's account. The Division further alleges that Wanger and Wanger Management failed to timely file required forms with Commission reporting purchases of securities as required by Section 16(a) of the Securities Exchange Act of 1934 and Rule 16a-3 thereunder.A hearing will be scheduled before an Administrative Law Judge to determine whether the allegations contained in the Order are true, and to provide the Respondents an opportunity to dispute these allegations, and to determine what, if any, remedial sanctions are appropriate and in the public interest.The Order requires the Administrative Law Judge to issue an initial decision no later than 300 days from the date of service of this Order, pursuant to Rule 360(a)(2) of the Commission's Rules of Practice. (Rels. 33-9288; 34-66053; IA-3342; IC-29893; File No. 3-14676)

2012: SEC Order Making Findings and Imposing Sanctions

Without admitting or denying the findings, Respondent Wanger and Respondent Wanger Investment Management submitted Offers of Settlement, which the SEC accepted. In the Matter of Eric David Wanger and Wanger Investment Management, Inc., Respondents. (Order Making Findings and Imposing Remedial Sanctions and a Cease-and-Desist Order Pursuant to Section 8a of the Securities Act, Section 21c of the Securities Exchange Act, Sections 203(E), 203(F), and 203(K) of the Investment Advisers Act of 1940, and Section 9(B) Of The Investment Company Act Of 1940; '33 Act Rel. No. 9331; '34 Act Rel. No. 67335; Invest. Adv. Act Rel. No. 3427; Invest. Co. Act Rel. No. 30126; Admin. Proc. File No. 3-14676 / July 2, 2012).

https://www.sec.gov/litigation/admin/2012/33-9331.pdf

As set forth, in part, in the Order Making Findings and Imposing Sanctions:

https://www.sec.gov/litigation/admin/2012/33-9331.pdf

As set forth, in part, in the Order Making Findings and Imposing Sanctions:

46. As a result of the conduct described above, Wanger willfully violated Sections 17(a)(1) and 17(a)(3) of the Securities Act, and Section 10(b) of the Exchange Act and Rule 10b-5 thereunder, which prohibit fraudulent conduct in the offer and sale of securities and in connection with the purchase or sale of securities.47. As a result of the conduct described above, Wanger Investment Management willfully violated Section 17(a)(1), 17(a)(2) and 17(a)(3) of the Securities Act, and Section 10(b) of the Exchange Act and Rule 10b-5 thereunder, which prohibit fraudulent conduct in the offer and sale of securities and in connection with the purchase or sale of securities.48. As a result of the conduct described above, Wanger willfully violated Section 16(a) of the Exchange Act and Rule 16a-3 thereunder, which require timely and accurate filings of Forms 4 with the Commission.49. As a result of the conduct described above, Wanger Investment Management willfully aided and abetted and caused the Fund's violations of Section 16(a) of the Exchange Act and Rule 16a-3 thereunder, which require timely and accurate filings of Forms 4 with the Commission.50. As a result of the conduct described above, Wanger and Wanger Investment Management willfully violated Section 206(3) of the Advisers Act, which states that it is unlawful for an investment adviser, "acting as principal for his own account, knowingly to sell any security to or purchase any security from a client . . . without disclosing to such client in writing before the completion of such transaction the capacity in which he is acting and obtaining the consent of the client to such transaction."51. As a result of the conduct described above, Wanger and Wanger Investment Management willfully violated Sections 206(1), 206(2) and 206(4) of the Advisers Act and Rule 206(4)-8 thereunder, which prohibit fraudulent conduct by an investment adviser.52. As a result of the conduct described above, Wanger willfully aided and abetted and caused Wanger Investment Management's violations of Sections 206(1), 206(2) and 206(4) of the Advisers Act and Rule 206(4)-8 thereunder, which prohibit fraudulent conduct by an investment adviser.

Having set forth the violations, the SEC imposed the following:

In view of the foregoing, the Commission deems it appropriate and in the public interest to impose the actions agreed to in Respondents' Offers.Accordingly, pursuant to Section 8A of the Securities Act, Section 21C of the Exchange Act, Sections 203(e), 203(f), and 203(k) of the Advisers Act, and Section 9(b) of the Investment Company Act, it is hereby ORDERED that:A. Respondent Wanger shall cease and desist from committing or causing any violations and any future violations of Section 17(a) of the Securities Act, Sections 10(b) and 16(a) of the Exchange Act and Rules 10b-5 and 16a-3 thereunder, and Sections 206(1), 206(2), 206(3), and 206(4) of the Advisers Act and Rule 206(4)-8 thereunder.B. Respondent Wanger be, and hereby is: barred from association with any broker, dealer, investment adviser, municipal securities dealer, municipal advisor, transfer agent, or nationally recognized statistical rating organization; and prohibited from serving or acting as an employee, officer, director, member of an advisory board, investment adviser or depositor of, or principal underwriter for, a registered investment company or affiliated person of such investment adviser, depositor, or principal underwriter. with the right to apply for reentry after one (1) year to the appropriate self-regulatory organization, or if there is none, to the Commission.C. Any reapplication for association by the Respondent Wanger will be subject to the applicable laws and regulations governing the reentry process, and reentry may be conditioned upon a number of factors, including, but not limited to, the satisfaction of any or all of the following: (a) any disgorgement ordered against the Respondent Wanger, whether or not the Commission has fully or partially waived payment of such disgorgement; (b) any arbitration award related to the conduct that served as the basis for the Commission order; (c) any self regulatory organization arbitration award to a customer, whether or not related to the conduct that served as the basis for the Commission order; and (d) any restitution order by a self regulatory organization, whether or not related to the conduct that served as the basis for the Commission order.D. Respondent Wanger shall, within 15 days of the entry of this Order, pay a civil money penalty in the amount of $75,000 to the United States Treasury. If timely payment is not made, additional interest shall accrue pursuant to 31 U.S.C. 3717. Such payment shall be: (A) made by wire transfer, United States postal money order, certified check, bank cashier's check or bank money order; (B) made payable to the Securities and Exchange Commission; (C) hand delivered or mailed to the Securities and Exchange Commission, Office of Financial Management, 100 F St., NE, Stop 6042, Washington, DC 20549; and (D) submitted under cover letter that identifies Eric David Wanger as a Respondent in these proceedings, the file number of these proceedings, a copy of which cover letter and money order or check shall be sent to Robert J. Burson, Division of Enforcement, Securities and Exchange Commission, 175 W. Jackson Blvd., Suite 900, Chicago, IL, 60604.E. Respondent Wanger Investment Management shall cease and desist from committing or causing any violations and any future violations of Section 17(a) of the Securities Act, Sections 10(b) and 16(a) of the Exchange Act and Rules 10b-5 and 16a-3 thereunder, and Sections 206(1), 206(2), 206(3), and 206(4) of the Advisers Act and Rule 206(4)-8 thereunder.F. Respondent Wanger Investment Management is censured.G. Respondent Wanger Investment Management shall, within 15 days of the entry of this Order, pay disgorgement of $2,269.81 and prejudgment interest of $121.94 to the United States Treasury. If timely payment is not made, additional interest shall accrue pursuant to SEC Rule of Practice 600. Payment shall be: (A) made by wire transfer, United States postal money order, certified check, bank cashier's check or bank money order; (B) made payable to the Securities and Exchange Commission; (C) hand-delivered or mailed to the Securities and Exchange Commission, Office of Financial Management, 100 F St., NE, Stop 6042, Washington, DC 20549; and (D) submitted under cover letter that identifies Wanger Investment Management as a Respondent in these proceedings, the file number of these proceedings, a copy of which cover letter and money order or check shall be sent to Robert J. Burson, Division of Enforcement, Securities and Exchange Commission, 175 W. Jackson Blvd., Suite 900, Chicago, IL, 60604.

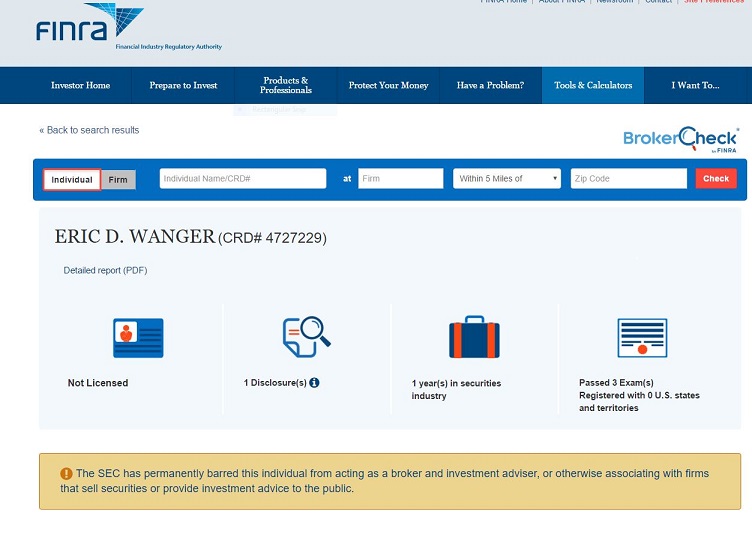

2016: BrokerCheck "Permanent Bar"

For all intents and purposes, the SEC case is over and we now move away from the federal regulator to a thorny issue involving the Financial Industry Regulatory Authority's ("FINRA's") BrokerCheck website. Assuming that you were perusing Eric Wanger's online BrokerCheck record as of June 9, 2016, this is what the opening page of his online file disclosed:

The SEC has permanently barred this individual from acting as a broker and investment adviser, or otherwise associating with firms that sell securities or provide investment advice to the public.

Permanent Bar Or a Bar With The Right To Reapply?

Before offering an opinion, re-read the applicable portion of the SEC's Order Making Findings and Imposing Sanctions:

A. Respondent Wanger shall cease and desist from committing or causing any violations and any future violations of Section 17(a) of the Securities Act, Sections 10(b) and 16(a) of the Exchange Act and Rules 10b-5 and 16a-3 thereunder, and Sections 206(1), 206(2), 206(3), and 206(4) of the Advisers Act and Rule 206(4)-8 thereunder.B. Respondent Wanger be, and hereby is: barred from association with any broker, dealer, investment adviser, municipal securities dealer, municipal advisor, transfer agent, or nationally recognized statistical rating organization; and prohibited from serving or acting as an employee, officer, director, member of an advisory board, investment adviser or depositor of, or principal underwriter for, a registered investment company or affiliated person of such investment adviser, depositor, or principal underwriter. with the right to apply for reentry after one (1) year to the appropriate self-regulatory organization, or if there is none, to the Commission.

Okay, so, Wanger is ordered to Cease-And-Desist and is "barred" with the "right to apply for reentry after one (1) year . . ."

Again, is that SEC-imposed Bar "permanent?" If you answer, "yes," then how do you explain the "right to apply for reentry after one (1) year?" I'm not saying that you can't rationalize a so-called "permanent" Bar with a right to apply for reentry. I'm just asking if the SEC confuses things by not characterizing the sanction as a "permanent bar," or, in the alternative, if FINRA is confusing things by making said characterization.

FINRA Alters and Reinterprets

If you ask Respondent Wanger, he would tell you that he is none too happy with FINRA's characterization of his SEC-imposed Bar as being permanent. In the Matter of the Application of Eric David Wanger. (Order Directing the Filing of Briefs, SEC, '34 Act Rel. No. 78019; Admin. Proc. File No. 3-17226 / June 8, 2016). https://www.sec.gov/litigation/opinions/2016/34-78019.pdf

As explained in pertinent part:

As explained in pertinent part:

[W[anger claims that the BrokerCheck posting "alter[s] the SEC Bar Order and re-interpret[s] the words . . . that now perforce has permanently blocked Respondent[] of his right to seek employment . . . ."At this time, the Commission requests the views of the parties as to the preliminary matter of whether the Commission has jurisdiction to review Wanger's application pursuant to Section 19 of the Securities Exchange Act of 1934 . . .

Ya gotta wonder. Was Rod Steward singing about "Forever Young" or did that come with an expiration date of, say, 21 years? And then, what about that iconic "Strawberry Fields Forever?" Did the Beatles really mean "forever" as in "permanent" or did they mean just for a long, long time?

2017: Not-so Permanent Bar

As of July 12, 2017, FINRA's online BrokerCheck records for Wanger disclosed:

BARREDThe SEC has barred this individual from acting as a broker or investment adviser or otherwise associating with firms that sell securities or provide investment advice to the public.

My, my, my . . . just what the hell happened with BrokerCheck's earlier "Permanent" Bar disclosure?

Lemme back in!

In April 2016, Wanger petitioned the SEC for reentry into the industry. Generally, at the time of requesting the ability to associate with a financial services firm, an applicant would present the name of the proposed employer and detail the proposed supervision under which employment would be pursued. Unfortunately for many folks who have been barred with a right to apply, brokerage firms, advisory firms, and other industry participants aren't typically lining up as a welcoming employer. In part, there is a belief by such firms that they will be tarred by the SEC as "bad boys" for hiring individuals who had previously been barred. Similarly, many potential employers will only make a contingent offer of employment -- which is often predicated with the requirement for the barred individual to first obtain reentry approval before any formal offer will be conveyed. As you may imagine, this regulatory setting tends to place reentry applicants in a frustrating loop that requires them to provide the name of an employer as part of their reentry application but they can't get a commitment from any employer until the SEC first approves their reentry. In Wanger's situation, the SEC's Bar with the right to apply after one year was imposed on July 2, 2012; and, accordingly, his right to apply for reentry after one year was activated in 2013. Now what?

SEC Rule of Practice 193

As is often the case, it's best to start with a consideration of the applicable SEC Rule pertaining to how a barred individual such as Wanger is required to pursue an application for reentry:

SEC Rule of Practice 193: Applications by barred individuals for consent to associate.Preliminary noteThis rule governs applications to the Commission by certain persons, barred by Commission order from association with brokers, dealers, municipal securities dealers, government securities brokers, government securities dealers, investment advisers, investment companies or transfer agents, for consent to become so associated. Applications made pursuant to this section must show that the proposed association would be consistent with the public interest. In addition to the information specifically required by the rule, applications should be supplemented, where appropriate, by written statements of individuals (other than the applicant) who are competent to attest to the applicant's character, employment performance, and other relevant information. Intentional misstatements or omissions of fact may constitute criminal violations of 18 U.S.C. 1001 et seq. and other provisions of law.The nature of the supervision that an applicant will receive or exercise as an associated person with a registered entity is an important matter bearing upon the public interest. In meeting the burden of showing that the proposed association is consistent with the public interest, the application and supporting documentation must demonstrate that the proposed supervision, procedures, or terms and conditions of employment are reasonably designed to prevent a recurrence of the conduct that led to imposition of the bar. As an associated person, the applicant will be limited to association in a specified capacity with a particular registered entity and may also be subject to specific terms and conditions.Normally, the applicant's burden of demonstrating that the proposed association is consistent with the public interest will be difficult to meet where the applicant is to be supervised by, or is to supervise, another barred individual. In addition, where an applicant wishes to become the sole proprietor of a registered entity and thus is seeking Commission consent notwithstanding an absence of supervision, the applicant's burden will be difficult to meet.In addition to the factors set forth in paragraph (d) of this section, the Commission will consider the nature of the findings that resulted in the bar when making its determination as to whether the proposed association is consistent with the public interest. In this regard, attention is directed to Rule 5(e) of the Commission's Rules on Informal and Other Procedures, 17 CFR 202.5(e). Among other things, Rule 5(e) sets forth the Commission's policy "not to permit a * * * respondent [in an administrative proceeding] to consent to * * * [an] order that imposes a sanction while denying the allegations in the * * * order for proceedings." Consistent with the rationale underlying that policy, and in order to avoid the appearance that an application made pursuant to this section was granted on the basis of such denial, the Commission will not consider any application that attempts to reargue or collaterally attack the findings that resulted in the Commission's bar order.(a) Scope of rule. Applications for Commission consent to associate, or to change the terms and conditions of association, with a registered broker, dealer, municipal securities dealer, government securities broker, government securities dealer, investment adviser, investment company or transfer agent may be made pursuant to this section where a Commission order bars the individual from association with a registered entity and:(1) Such barred individual seeks to become associated with an entity that is not a member of a self-regulatory organization; or(2) The order contains a proviso that application may be made to the Commission after a specified period of time.(b) Form of application. Each application shall be supported by an affidavit, manually signed by the applicant, that addresses the factors set forth in paragraph (d) of this section. One original and three copies of the application shall be filed pursuant to §§201.151, 201.152 and 201.153. Each application shall include as exhibits:(1) A copy of the Commission order imposing the bar;(2) An undertaking by the applicant to notify immediately the Commission in writing if any information submitted in support of the application becomes materially false or misleading while the application is pending;(3) The following forms, as appropriate:(i) A copy of a completed Form U-4, where the applicant's proposed association is with a broker-dealer or municipal securities dealer;(ii) A copy of a completed Form MSD-4, where the applicant's proposed association is with a bank municipal securities dealer;(iii) The information required by Form ADV, 17 CFR 279.1, with respect to the applicant, where the applicant's proposed association is with an investment adviser;(iv) The information required by Form TA-1, 17 CFR 249b.100, with respect to the applicant, where the applicant's proposed association is with a transfer agent; and(4) A written statement by the proposed employer that describes:(i) The terms and conditions of employment and supervision to be exercised over such applicant and, where applicable, by such applicant;(ii) The qualifications, experience, and disciplinary records of the proposed supervisor(s) of the applicant;(iii) The compliance and disciplinary history, during the two years preceding the filing of the application, of the office in which the applicant will be employed; and(iv) The names of any other associated persons in the same office who have previously been barred by the Commission, and whether they are to be supervised by the applicant.(c) Required showing. The applicant shall make a showing satisfactory to the Commission that the proposed association would be consistent with the public interest.(d) Factors to be addressed. The affidavit required by paragraph (b) of this section shall address each of the following:(1) The time period since the imposition of the bar;(2) Any restitution or similar action taken by the applicant to recompense any person injured by the misconduct that resulted in the bar;(3) The applicant's compliance with the order imposing the bar;(4) The applicant's employment during the period subsequent to imposition of the bar;(5) The capacity or position in which the applicant proposes to be associated;(6) The manner and extent of supervision to be exercised over such applicant and, where applicable, by such applicant;(7) Any relevant courses, seminars, examinations or other actions completed by the applicant subsequent to imposition of the bar to prepare for his or her return to the securities business; and(8) Any other information material to the application.(e) Notification to applicant and written statement. In the event an adverse recommendation is proposed by the staff with respect to an application made pursuant to this section, the applicant shall be so advised and provided with a written statement of the reasons for such recommendation. The applicant shall then have 30 days to submit a written statement in response.(f) Concurrent applications. The Commission will not consider any application submitted pursuant to this section if any other application for consent to associate concerning the same applicant is pending before any self-regulatory organization.

2017: SEC Denies Wanger's Application for Association

By way of spoiler alert, the SEC denied Wanger's application for association. As set forth in the Syllabus to In the Matter of the Application of Eric David Wanger. (Order Denying Application for Consent to Associate, '34 Act Rel. No. 81111; Invest. Adv. Act Rel. No. 4728; Admin. Proc. File No. 3-14676 / July 10, 2017)

http://brokeandbroker.com/PDF/WangerSECOrdDeny170710.pdf [Ed: footnotes omitted]:

http://brokeandbroker.com/PDF/WangerSECOrdDeny170710.pdf [Ed: footnotes omitted]:

In placing Wanger's application in context, the SEC Order Denying states [Ed: footnotes omitted]:Eric David Wanger was the owner, chief compliance officer, and president of Wanger Investment Management, Inc. ("WIM"), a formerly Commission-registered investment adviser. In order to settle administrative and cease-and-desist proceedings brought against him, Wanger consented to a Commission order that, among other sanctions, barred him from the securities industry with a right to apply for reentry after one year. He now has filed an application for consent either to (1) associate with any registered or unregistered broker-dealer, investment adviser, or other entity that participates in the securities industry or (2) establish his own entity that provides one or more of those services. He submits this application under both Rule 193 of the Commission's Rules of Practice and Section 203(f) of the Investment Advisers Act of 1940. For the reasons set forth below, we conclude that Wanger has failed to show that the proposed terms of reentry would be consistent with the public interest. Accordingly, his application is denied.

Page 3 of the SEC Order DenyingOn April 20, 2016, through new counsel, Wanger filed an application, later supplemented, seeking "consent to re-enter the securities industry either to (1) associate with any registered or unregistered broker-dealer, investment adviser, or other entity that participates in the securities industry, or (2) establish his own entity that provides one or more of these services."The application provides no information about the entities with which Wanger proposes to associate or establish, what activities they do or would engage in, what activities Wanger would engage in, or what supervision, if any, would be exercised over or by him. Wanger explains this failure by asserting that the bar has made it "impossible" for him to find a firm to sponsor his application or agree to supervise his activities, and he therefore contends that the requirements for reentry under Commission Rule of Practice 193 and Advisers Act Section 203(f) are "incapable of being fulfilled."In lieu of providing the information that Rule 193 requires about the proposed association and supervision, Wanger devotes the bulk of his application and supporting materials to challenging the fairness of the underlying proceeding prior to the settlement and the fairness of the terms of the settlement to which he agreed. The application also describes Wanger's purported understanding that he would have the right to reenter the securities industry after one year, rather than the right to apply for reentry subject to our discretion. Wanger further criticizes a posting on FINRA's BrokerCheck website that he asserts mischaracterized our bar order.

The SEC Order Denying reiterates the SEC's position that whether a proposed association is consistent with the public interest requires an examination of a proposed employer's background with a focus on the proposed supervisory structure. In undertaking that analysis, the SEC asserts that: [Ed: footnotes omitted]:

Pages 5 -6 of the SEC Order DenyingWanger does not address either of these factors in his application. He does not identify a proposed employer, the terms and conditions of his planned employment, or the supervision, if any, that would be exercised over him in his new position. He does not say what he would be doing, for whom (if anyone) he would be doing it, or how he would be interacting with clients, investors, or other market participants. Instead, his application seeks our consent to "associate with any registered or unregistered broker-dealer, investment adviser, or other entity that participates in the securities industry" or, failing that, to "establish his own entity that provides one or more of those services." Such a general, unconditional request is inconsistent with the carefully tailored reentry conditions that Rule 193 contemplates. Wanger's application offers no evidence that his unidentified future activities would be conducted in a manner designed to "prevent a recurrence of the conduct that led to the imposition of the bar" in the first place, and provides us with no basis on which to conclude that granting his request would be "consistent with the public interest."Wanger's request is functionally equivalent to asking us to vacate the bar entirely and free him from any restrictions or oversight on his future activities. But that is extraordinary relief that we grant only under the most "compelling circumstances," and Wanger's application fails to present any such circumstances. Although Wanger contends that the bar has made it "impossible" for him to identify a sponsoring firm and thus satisfy Rule 193's requirements, difficulty finding suitable employment is "among . . . the natural and foreseeable consequences that flow from a ban on employment in the securities industry."It is not a "compelling circumstance" that would justify wholly vacating a remedial sanction designed to prevent recurrence of misconduct and protect investors and the integrity of the markets. Wanger has failed to carry his burden of showing that the requested relief would be consistent with the public interest and, accordingly, his request should be denied.

Also READ: "In S.E.C.'s Streamlined Court, Penalty Exerts a Lasting Grip / A money manager settled his case with the S.E.C. thinking he could go back to work in a year. Nearly five years later, he is still waiting" (New York Times, by Gretchen Morgenson / May 4, 2017)

https://www.nytimes.com/2017/05/04/business/sec-internal-court.html

2020: SEC Grants Consent to Associate

Wanger filed an application for consent to associate with Burling Acquisition Group, LLC, which intends to form an exempt, unregistered private equity fund (De Novo Fund, LLC.) for which Burling will act as the adviser --and the formation of the Fund is contingent upon the SEC's granting Wanger consent to associate with Burling because such consent is required per the firm's role as the Fund's proposed investment adviser. In the Matter of an Application Filed Under Rule 193 of the Commission's Rules of Practice and Section 203(f) of the Investment Advisers Act on behalf of ERIC D. WANGER For Consent to Associate with Burling Acquisition Group, LLC (SEC Order Granting Consent to Associate, Invest. Adv. Act Rel. No. 5621; Admin. Proc. File No. 3-14676 / October 26, 2020) (the "2020 SEC Order to Associate")

https://www.sec.gov/litigation/admin/2020/ia-5621.pdf

In granting Wanger its consent for his proposed association with Burling, the 2020 SEC Order to Associate states in part that:

Mr. Wanger's Application seeks Commission consent to his association with Burling, which intends to act as general partner and investment adviser to the Fund.2 With respect to the Fund, Mr. Wanger's role will be limited to identifying investments in private companies and qualified purchasers for it. The Application represents that Mr. Wanger is a manager and member of Burling with a 43.5% ownership interest and will be supervised by Stuart Schwartz, a manager and a member of Burling. Burling will impose supervisory restrictions, including the following: (i) Burling will not engage in securities transactions on secondary markets and Mr. Wanger will not trade on Burling's behalf; (ii) all investor-related agreements requiring execution by Burling must be approved and signed by Mr. Schwartz; (iii) Burling will not hold or custody any of the Fund's cash or assets as these will all be handled by a third-party administrator and Mr. Wanger will therefore not be required or permitted to handle client cash or Fund assets; (iv) Mr. Wanger will have no role in valuing the Fund's assets for reporting and fee computation purposes, and Burling will value all assets either at cost or at a specific value provided at arms-length by a third-party valuation firm; and (v) Burling and the Fund will be audited annually by an audit firm registered with the Public Company Accounting Oversight Board. The Application further represents that neither Mr. Schwartz nor Burling has a disciplinary history.In reliance upon the representations made by Mr. Wanger and Burling, the Commission has concluded that the applicant has made a satisfactory showing that the proposed association is consistent with the public interest.The Commission's consent permits Mr. Wanger to associate with Burling in its capacity as an investment adviser to the Fund, limited to the terms of association described in this order. If Mr. Wanger seeks to associate in any other capacity, a new application must be made.Mr. Wanger shall certify annually that he has complied with this Order Granting Consent to Associate. This certification requirement expires five years from the date of this Order. The certification shall be submitted to the Office of Chief Counsel of the Commission's Division of Enforcement. . . .= = = = =Footnote 2: The Application represents that the Fund will not make any public offering of its securities and will limit its owners to "qualified purchasers" as defined by Section 2(a)(51)(A) of the Investment Company Act, 15 U.S.C. 80a2(a)(51)(A); consequently, the Fund will not be an investment company within the meaning of that act, as provided by Section 3(c)(7), 15 U.S.C. 80a-(3)(7). The Application further represents that Burling will act solely as the adviser to the Fund, and will have less than $150 million under management; consequently, Burling will not be required to register as an investment adviser, pursuant to the registration exemption in Section 203(m)(1) of the Investment Advisers Act, 15 U.S.C. 80b-3(m)(1).