PNC Loses Wrongful Termination FINRA Arbitration

September 1, 2017

Today's BrokeAndBroker.com Blog features an intra-industry employment dispute involving allegations of defamation, libel, slander, and wrongful termination. The former employee took exception with his former employer's characterization that he had been terminated because of his inappropriate behavior. In stark contrast to the employer's allegation, the employee argued that he was retaliated against after complaining about sexual harassment. There are lots of aspects of this FINRA arbitration that should catch the eye of both lawyers and industry participants. For one thing, it took over five years from the date of termination until the rendering of the FINRA Arbitration Decision. For another thing, the employer has a history of former-employee lawsuits alleging similar claims of improper disclosures.

Case In Point

In a Financial Industry Regulatory Authority ("FINRA") Arbitration Statement of Claim filed in August 2013, and as amended thereafter, Claimant Walter asserted defamation; libel and slander on his Form U5; tortious interference with prospective economic advantage; and wrongful termination. Claimant alleged that after he had complained about sexual harassment, he was wrongfully terminated based on Respondent PNC's allegations of inappropriate behavior. In addition to seeking an expungement, at the close of the hearing, Claimant sought at least $225,416 in special damages and lost wages; $2,479,576.00 in punitive damages; costs, and fees. In the Matter of the FINRA Arbitration Between Jeffrey J. Walter, Claimant, vs. PNC Investments, LLC, Respondent (FINRA Arbitration # 13-02391, August 18, 2017).

Respondent PNC generally denied the allegations and asserted various affirmative defenses.

Award

The FINRA Arbitration Panel found Respondent PNC liable and ordered it to pay to Claimant Walter $290,485.00 in compensatory damages plus 6% per annum interest until paid in full.

The Panel deemed that the U5 disclosure at issue was defamatory. Although the arbitrators declined to recommend the expungement of the Form U5 "Reason for Termination," they recommended the expungement of the Form U5 by proposing the revision from "YES" to "NO" of question 7(F)(1) with the deletion of the accompanying "Termination Disclosure Report Page." The Panel further recommended the expungement of the Form U5 via a proposed revision of the "Termination Explanation" as follows:

Jeffery J. Walter was terminated for a violation of an internal code of conduct. No securities or securities customers were involved in this matter.

SIDE BAR: The applicable questions on the Uniform Termination Notice for Securities Industry Registration ("Form U5"):3. FULL TERMINATIONIs this a FULL TERMINATION?Note: A "Yes" response will terminate ALL registrations with all SROs and all jurisdictions.Reason For Termination:[]Discharged []Other []Permitted to Resign []Deceased []VoluntaryTermination Explanation:If the Reason for Termination entered above is Permitted to Resign, Discharged or Other, provide an explanation below:If amending the Reason for Termination and/or termination explanation, provide an explanation below:. . .Termination Disclosure7F. Did the individual voluntarily resign from your firm, or was the individual discharged or permitted to resign from your firm, after allegations were made that accused the individual of:1. violating investment-related statutes, regulations, rules or industry standards of conduct?2. fraud or the wrongful taking of property?3. failure to supervise in connection with investment-related statutes, regulations, rules or industry standards of conduct?

Bill Singer's Comment

Truly, I have no idea what the precipitating incident(s) was here from a reading of this FINRA Arbitration Decision. FINRA's online BrokerCheck records as of September 1, 2017, disclose that Walter had been "discharged" by PNC on August 15, 2012. I would urge all readers to focus on that date: It took Walter over five years to obtain some redress of his disputed termination -- and counting from the date of his filing of his claims in 2013, the FINRA arbitration process required over four years to reach the Award stage.

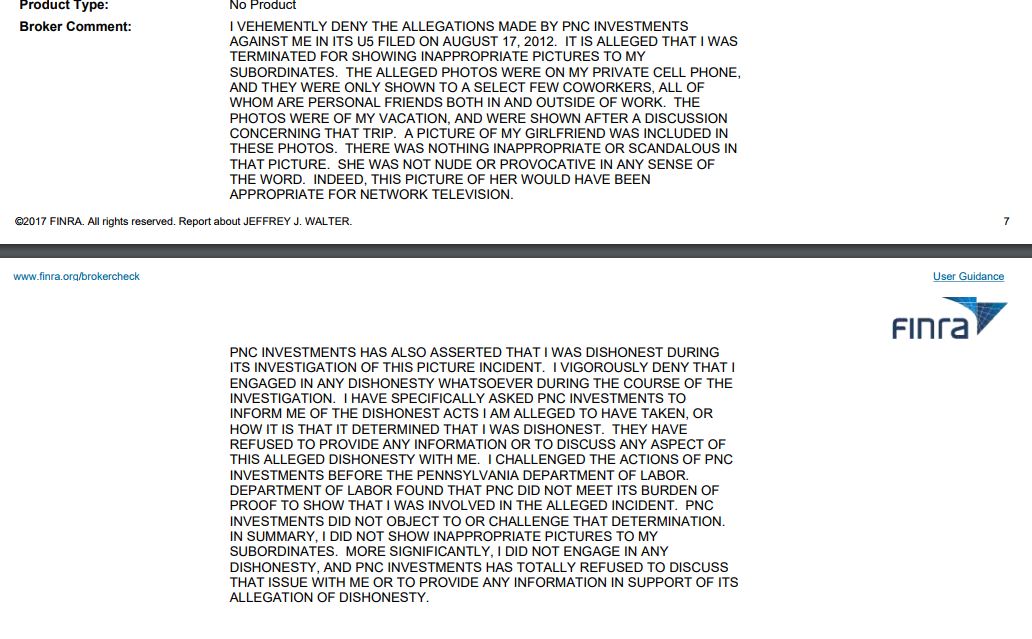

Walter's BrokerCheck Comment

In trying to make some sense of the underlying events, consider the screenshot below of Walter's "Broker Comment" on BrokerCheck in response to PNC's allegations concerning his discharge:

"PNC and Wells Fargo Stockbroker Wins Customer Complaints Expungement" (BrokeAndBroker.com Blog, September 19, 2016):Claimant asserted PNC Investments failed to investigate the customer's allegation with due diligence, that the allegation and claim are false, and finally that he was not involved with the alleged misconduct. He presented proof supporting this position during his testimony at the hearings.""Defamed PNC Employee Wins Dramatic Expungement" (BrokeAndBroker.com Blog, September 20, 2016):

[T]he Panel recommends that the language be expunged in its entirety and replaced with the following language: "A FINRA arbitration panel determined that the termination of John Gross by PNC Investments was arbitrary and unreasonable."

"Veteran Wall Street Critic Bill Singer Slams FINRA Expungement Process" (BrokeAndBroker.com Blog, October 17, 2016):The Panel found that the cited language placed by PNC on Kost's Form U5 was defamatory. The Panel retained the Form U5 "Reason for Termination" but recommended the deletion of the "Termination Explanation" in Section 3 of Claimant Shawn Kost's Form U5 filed by PNC on December 17, 2014. The Panel recommended that the explanation be revised to:

Sean Kost was terminated by PNC Investments as an at will employee without cause, but due to management decisions made.

FINRA Rule 2080. Obtaining an Order of Expungement of Customer Dispute Information from the Central Registration Depository (CRD) System(a) Members or associated persons seeking to expunge information from the CRD system arising from disputes with customers must obtain an order from a court of competent jurisdiction directing such expungement or confirming an arbitration award containing expungement relief.(b) Members or associated persons petitioning a court for expungement relief or seeking judicial confirmation of an arbitration award containing expungement relief must name FINRA as an additional party and serve FINRA with all appropriate documents unless this requirement is waived pursuant to subparagraph (1) or (2) below.

(1) Upon request, FINRA may waive the obligation to name FINRA as a party if FINRA determines that the expungement relief is based on affirmative judicial or arbitral findings that:

(A) the claim, allegation or information is factually impossible or clearly erroneous;(B) the registered person was not involved in the alleged investment-related sales practice violation, forgery, theft, misappropriation or conversion of funds; or(C) the claim, allegation or information is false.

(2) If the expungement relief is based on judicial or arbitral findings other than those described above, FINRA, in its sole discretion and under extraordinary circumstances, also may waive the obligation to name FINRA as a party if it determines that:

(A) the expungement relief and accompanying findings on which it is based are meritorious; and(B) the expungement would have no material adverse effect on investor protection, the integrity of the CRD system or regulatory requirements.

(c) For purposes of this Rule, the terms "sales practice violation," "investment-related," and "involved" shall have the meanings set forth in the Uniform Application for Securities Industry Registration or Transfer ("Form U4") in effect at the time of issuance of the subject expungement order.

FINRA Rule 1122. Filing of Misleading Information as to Membership or Registration

No member or person associated with a member shall file with FINRA information with respect to membership or registration which is incomplete or inaccurate so as to be misleading, or which could in any way tend to mislead, or fail to correct such filing after notice thereof.

FINRA Rule 2010. Standards of Commercial Honor and Principles of Trade

A member, in the conduct of its business, shall observe high standards of commercial honor and just and equitable principles of trade.

READ the BrokeAndBroker.com Blog Expungement Archive