FINRA Arbitrator Unimpeded By Defaulting Brokerage Firm

September 13, 2017

If you work on Wall Street, chances are that you're forced to arbitrate most disputes before the Financial Industry Regulatory Authority ("FINRA"). Given the nature of arbitration as frequently affirmed by the courts, it's viewed as a so-called alternative dispute resolution ("ADR") process unencumbered by all of the due process rights that are inherent in our court system. For staunch advocates of free enterprise, arbitration exalts the rights of individuals to pursue their grievances via a contractually negotiated process that promises to be quicker, cheaper, and more confidential that civil litigation in the courts. As with many things in life, promises are not always realized.

My personal view of arbitration has been expressed many times on the BrokeAndBroker.com Blog. Simply stated, I am a libertarian with a small "l" and take no issue with the ability of parties to freely negotiate any agreement that provides for the fair resolution of disputes via ADR. What I detest is any mandatory system of arbitration that is the byproduct of non-negotiable contracts and tainted by the appearance of undue influence exercised in the rulemaking process and funding of the arbitration forum. By way of making my point, see if you can get a job on Wall Street without being subjected to the industry's system of mandatory arbitration; and, similarly, try to open a brokerage account without agreeing to the mandatory customer arbitration clause. Where in any of that take-it-or-leave-it is there a freely negotiated contract to arbitrate? Setting that rant aside for the moment, let's consider a recent intra-industry FINRA arbitration and the extent to which the rendered decision satisfies our concerns for fairness.

Case In Point

In a Financial Industry Regulatory Authority ("FINRA") Arbitration Statement of Claim filed in December 2016, associated person Claimant Knight sought an expungement of information filed by his former employer Respondent Hudson Knight Securities. As set forth in pertinent part in the FINRA Arbitration Decision, Claimant Knight alleged that:

his business partner fraudulently used Claimant's identity to open a corporate credit card and a cellular phone account for Respondent. Claimant asserted that, after he confronted his business partner, Respondent terminated Claimant and filed a Form U5 including false allegations surrounding the circumstances of Claimant's termination.

In the Matter of the FINRA Arbitration Between Calvin Courtney Knight, Claimant, vs. Hudson Knight Securities, Inc., Respondent (FINRA Arbitration 16-03550, September 1, 2017).

Respondent Hudson Knight Securities did not file an Answer and did not appear at the hearing.

SIDE BAR: A former partner, identity theft, a credit card account, and a cellphone account . . . wow, you don't see that every day. I sort of wish that the FINRA Arbitration Decision gave us more of a fact pattern because there is no indication as to when any of the cited events took place. Also, I'm guessing that Claimant Knight may have been the "Knight" in "Hudson Knight Securities," but that's not confirmed anywhere in the Decision. Similarly, the "business partner" at the heart of Claimant's case is never named by name in the Decision and there is no explanation in the Decision as to whether Claimant and the "business partner" were the owners of "Hudson Knight Securities." Finally, the Decision does not state whether the "business partner" was the individual who filed the disputed Form U5 or if someone filed the regulatory form at the behest of that partner. As such, if you're playing along at home, it's not you (and it's not me) -- it is, in fact, a lack of content and context in this FINRA Arbitration Decision.

Default

Whatever my pissy and annoyed quibbles with what's not in the FINRA Arbitration Decision, I don't expect any major issues with the outcome of the case because, frankly, there's no way that Claimant Knight is going to lose his case. I say that because Respondent Hudson Knight Securities was a no-show, as in the firm did not execute a Uniform Submission Agreement, did not file an Answer, and did not send a representative to contest any aspect of Claimant's allegations. Moreover, by Order dated April 4, 2017, the FINRA Arbitration Chairperson granted Claimant's request to deem the case as a "default proceeding" (and the Chairperson became the sole FINRA Arbitrator). Finally, the sole FINRA Arbitrator found that "Respondent is a defunct entity that is no longer registered with FINRA."

Unimpeded

And so we move forward to the default hearing. At the hearing, Claimant's allegations against his former employer Respondent will be unrefuted because that firm is a no-show, defunct, and no longer FINRA-registered. As such, all that the Claimant has to do is show up, present his proof, give his testimony, and smile as no one cross examines him or offers any opposing evidence. In light of that, consider this finding by the Arbitrator:

[T]he Arbitrator has determined that, since he finds that Claimant has failed to meet his burden of proof for expungement, the failure of Respondent to participate did not impede the Arbitrator in evaluating Claimant's case.

Accordingly, the sole FINRA Arbitrator denied all of Claimant's claims and request for expungement.

Bill Singer's Comment

Are you f#@king kidding me? Seriously?? I mean, really???

The "failure of Respondent to participate did not impede the Arbitrator in evaluating Claimant's case?" I mean, sure, okay, as a lawyer with some 32 years of practice I understand that even in a default case a Claimant has the burden of proof. In this case, however, how the hell did the sole FINRA Arbitrator reject Claimant's uncontroverted allegations?

- There was no Answer asserting anything to the contrary of Claimant's claims.

- There was no witness contradicting Claimant.

- There were no documents introduced by Respondent that disputed any allegation by Claimant.

An Unappealing Case

Now, let me be very, very clear here. It may well be that this sole FINRA Arbitrator heard Claimant's testimony and reviewed with great attention to detail all of Claimant's evidence, and notwithstanding the absence of any argument to the contrary from a defaulting Respondent, this same Arbitrator came away convinced that even the most cursory burden of proof was not satisfied. That happens and in such a case, a dismissal is appropriate. Nonetheless, in a default FINRA Arbitration with no appearance or filed Answer by a defunct member firm, FINRA must require some substantive explanation as to why an arbitrator(s) denied the claims. It is not enough to publish a conclusory explanation that the Claimant didn't carry the burden of proof.

Claimant Knight may well want to appeal this Decision to the courts for purposes of having it vacated and gaining a new hearing. You tell me the bases for Claimant's appeal. You tell me how a judge is going to determine whether this Arbitrator did or did not render a sustainable verdict. FINRA's failure to impose some quality control on the content and context presented in its Decisions not only places the litigating parties in difficult postures should they decide to file an appeal with the courts but also places the arbitrators in unflattering roles.

When?

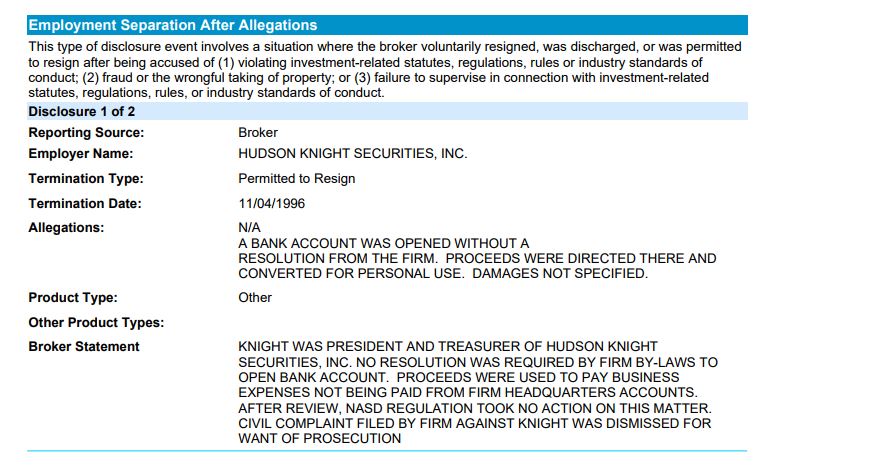

On what dates did the underlying events in this dispute occur? You're not going to find any dates pertaining to the former partner, identity theft, credit card account, and cellphone account allegations because the FINRA Arbitration Decision does not state any. As such, take a guess. When do you think the underlying acts took place?

According to online FINRA BrokerCheck records as of September 13, 2017, Claimant Knight was first registered in 1986 and was only registered with Respondent Hudson Knight from August 1995 to December 1996! If Claimant was no longer with Respondent as of 1996, then we must infer that the conduct at issue in the arbitration is at least 21 years old. As to why Claimant waited some 21 years to seek an expungement is yet another baffling and unexplained aspect of this baffling and inexplicable arbitration.

Finding myself so angered by this abortion of a Decision and so aghast at the lack of facts and rationale, I will simply post a screenshot of the pertinent portion of FINRA's online BrokerCheck record: Download a PDF copy of Bill Singer Esq's analysis of FINRA's Expungement Rules

Download a PDF copy of Bill Singer Esq's analysis of FINRA's Expungement Rules